The economic conditions surrounding future interest rate hikes, which could put renewed pressure on valuations, complicate loan refinancing, and impede debt servicing could cause major dislocation in commercial real estate markets. JGM Properties highlights relevant insights below.

Despite recent bipartisan cooperation on the federal budget, debt ceiling, and a brightening economic outlook, various policy risks such as the scheduled sunset of the Terrorism Risk Insurance Act (TRIA) on December 31st continue to weigh on real estate markets. These could spark a job-killing commercial real estate credit crunch. (cited source: http://www.cbre.us/o/minneapolis/AssetLibrary/MSP Market Outlook 2014%5B2%5D.pdf)

“If the statistics detailing the debt and structured finance outlook for commercial real estate in 2014 are anything to go by, it clearly shows that refinancing might be the immediate need of the hour,” said Eli Russell, Leasing & Marketing Manager with JGM Properties.

According to Gregory Michaud, Senior Vice President, Head of Real Estate Finance at ING, “Commercial real estate debt on a broadly diversified portfolio of stabilized, multi-tenant properties will produce superior risk-adjusted fixed income returns through consistent income generation, preservation of principal and low volatility.” (cited source: http://www.inginvestment.com/Institutional/Investment-Capabilities/Fixed-Income/Commercial-Real-Estate-Debt/index.htm?tab=Overview)

The Real Estate Roundtable’s latest quarterly Sentiment Survey, released recently indicates that U.S. commercial real estate markets are continuing their gradual recovery from recession. Improving fundamentals, transaction volumes, and capital flows, especially in non-gateway markets indicate this. Over the coming year, it will likely remain on a modestly upward trajectory. (cited source: http://www.prnewswire.com/news-releases/commercial-real-estate-execs-more-confident-although-headwinds-remain-246362411.html). The commercial real estate industry generally has stabilized, and is poised to lead the economy forward once again in the areas of job growth, GDP, tax revenue, and retiree investments held by U.S. pension funds. However, refinancing may be the last resort unless the government provides more clarity on key policies, fosters appropriate risk-taking and entrepreneurial activity, enacts positive, pro-growth reforms in the tax, immigration, and energy policy spheres, and protects U.S. economic and homeland security.

Chairman, president and CEO of Michigan-based Taubman Centers Inc. said, “The slight uptick in our latest Sentiment Index shows our industry on a generally positive path in keeping with broader macroeconomic trends yet still not fully recovered, and still subject to policy-related risks.”

“U.S. policymakers must work to create a more attractive climate for job creation and investment as these are critical to real estate’s health — and as real estate goes, so goes the economy,” added Taubman, whose firm owns an international portfolio of regional and super regional malls.

Research by property consultancy, CBRE shows there is €926bn (£762bn) of outstanding commercial real estate (CRE) debt across Europe. With this being just 11% lower than the level seen at the peak of the financial crisis in 2008, this goes to show how the European commercial real estate market is still up to its eyeballs in debt. (cited source: http://www.cityam.com/blog/1390921143/european-commercial-real-estate-market-swimming-debt)

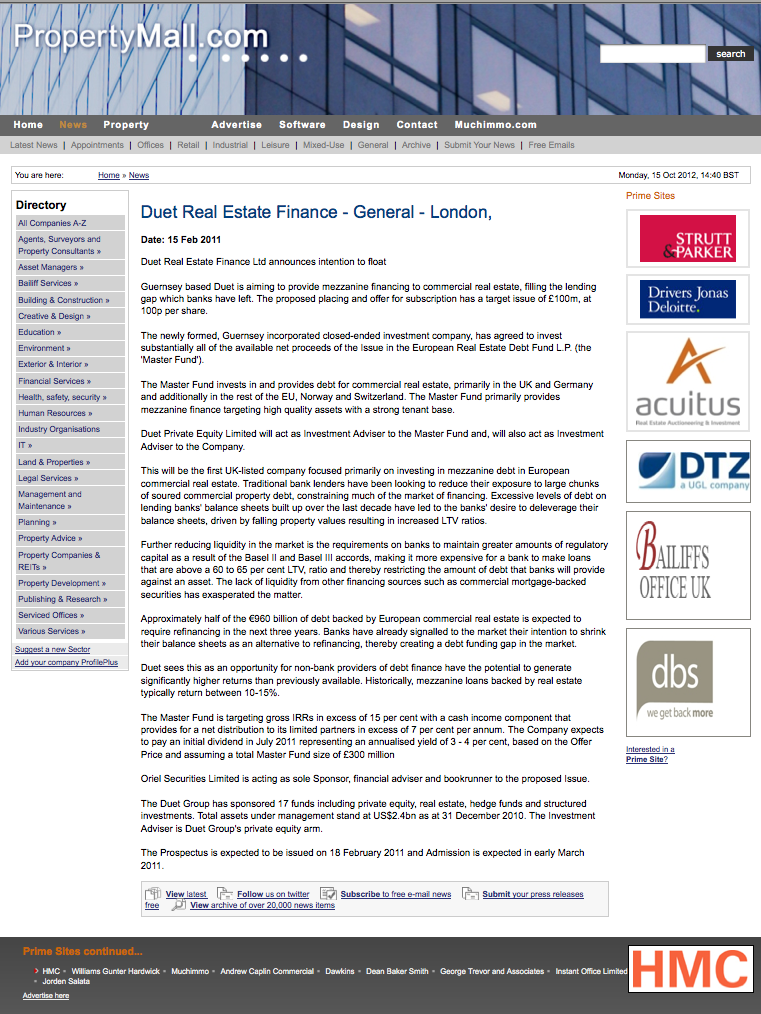

PropertyMall, a UK based commercial real estate news company lends their insight back in February 2011 (original post from 2011 is no longer active; but I located a screen shot of the original post…see image snap-shot of PropertyMall article below).

So, unless new lenders such as insurers ramp up their activity, a large chunk of this is unlikely to meet its maturity deadlines unless. 79% (€731bn) of the total outstanding debt is due to mature in the next five years. 24% (€244bn) of the debt that existed at the end of 2008 has now been retired and 15% of the total is from debt that has been issued against new commercial property deals since the end of 2008 per CBRE estimates. In Europe, new lenders, such as debt funds, insurers, private equity and capital markets have not yet entered the market to the level required to make a significant impact as they are still very much in their infancy. Until the ‘new lenders’ enter the market in earnest, many Eurozone banks will continue to retain a large debt overhang, and there is unlikely to be enough debt retired to hit maturity deadlines.

Good insight here into commercial real estate debt in Minnesota and beyond. There are strong reasons for investors to become involved. Right now, there is a high demand for capital, but limited availability. So, this creates some interesting opportunities until lending and refinancing has been freed up. The situation in Europe is also an important factor to keep an eye on. As you said, the situation there is even worse. I’d be interested to see you continue to provide analysis on this issue, particularly as it continues to effect commercial real estate MN and in the Midwest.